NYS Mansion & Transfer Tax Changes: What Buyers Need to Know

Real Estate Claudia Saez-Fromm October 10, 2022

Real Estate Claudia Saez-Fromm October 10, 2022

The good news:

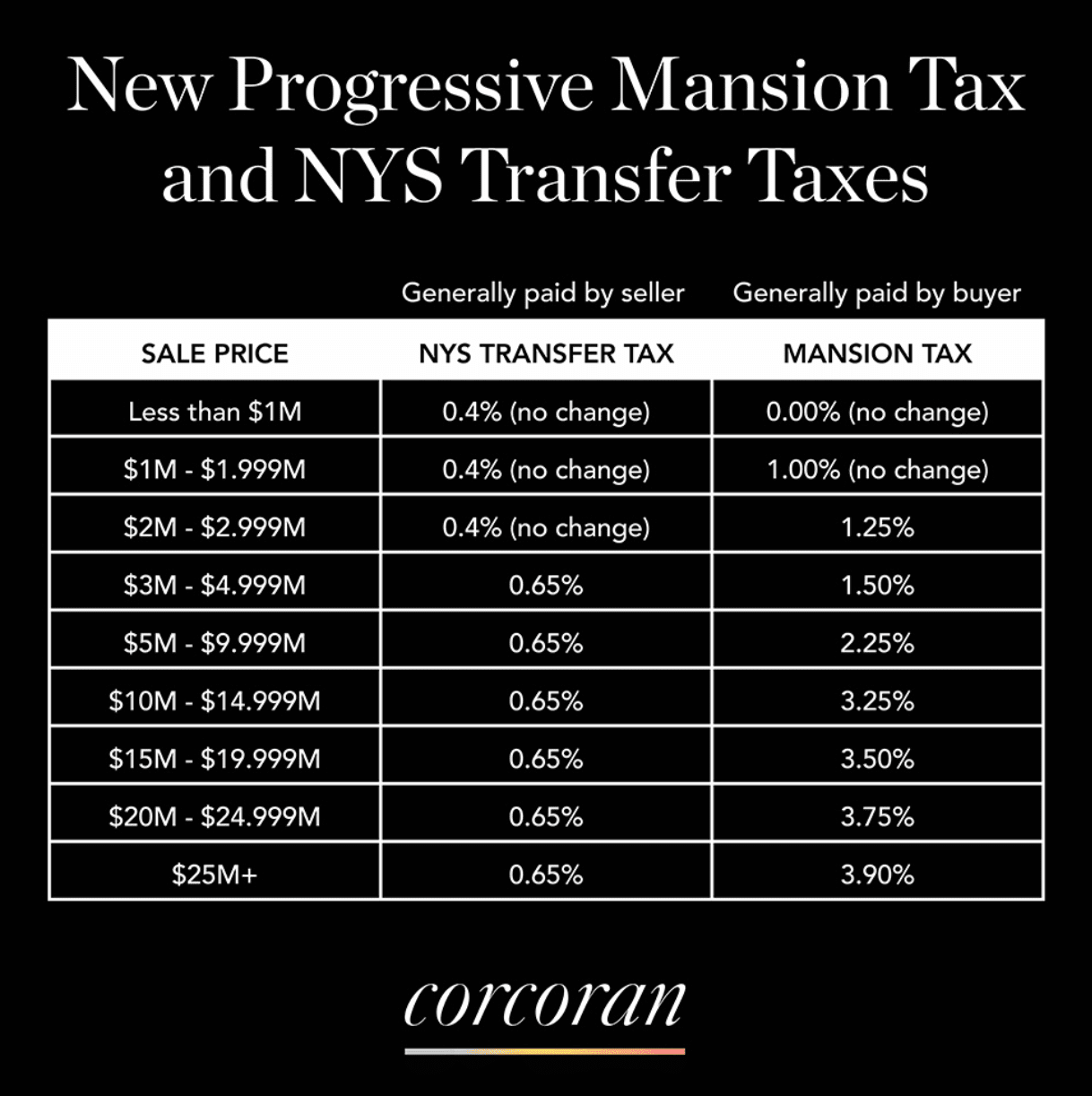

There is NO pied a terre tax. The ONLY changes are to the NYS transfer tax for residential sales above $3M, and to the mansion tax for sales at and above $2M, which is going up by increasing margins dependent on the sale price. These are one-time (not recurring) transaction costs incurred at the time of purchase. The funds raised are being used to improve and upgrade the NYC transit system which is in desperate need of investment, as we all know.

The upshot:

Practically speaking, there is a 25 basis point (one quarter percent) increase to the NYS transfer tax for sales above $3M; this represents a roughly 14% increase over the current level. Note: There is no change to the NYC transfer tax which remains 1.425% for sales greater than $500,000 (1% for sales less than or equal to $500,000).

Timing:

The tax act takes effect on July 1, 2019, and applies to any sales closing on or after that date. However, if a contract was signed before April 1, 2019, and closes on or after 7/1/2019, then the new taxes will NOT apply, i.e. these deals will be grandfathered under the prior code. A deal entered into now and closed before July 1, 2019, would also be exempt.

The actual changes are summarized below:

New NYS Transfer Tax of of 0.65%:

Stay up to date on the latest real estate trends.

June 18, 2026

June 11, 2026

June 4, 2026

May 28, 2026

May 21, 2026

May 14, 2026

May 7, 2026

April 23, 2026

April 16, 2026

As a top team at Douglas Elliman, SAEZFROMM continues to deliver the greatest value to our buyers, sellers, developers, and investors. Our focus is on one thing above all others: our clients, their needs, and what makes them happy.

SAEZFROMM

M: (212) 203-1798

O: (212) 891-7181

[email protected]

Douglas Elliman Real Estate

140 Franklin St

New York NY 10013